Março de 2020 será uma data memorável no calendário de títulos dos EUA. Vimos essa onda nas duas primeiras semanas de março de 2020, primeiro a partir da pandemia Covid 19 e depois o colapso do preço do petróleo causado pelo impasse entre a Arábia da Saudia e a Rússia

A relação entre o preço de um título e as taxas de juros prevalecentes || 188

Consider a two year 10% Treasury note issued by the US government. The £100 is known as the face value of the note and the interest rate attached to the note is known as the coupon rate. The government will pay £10 semi-annually for two years, and £100 at the end of the two-year term. Assume, also that other similar securities are providing a return of 10%. if one does the maths and were to discount back each of these cash flows, we would find that the price of the bond will be equal to £100. In other words, if the prevailing interest rate (yield) is equal to the coupon rate, the price of the bond or fair value will equal the face value and is said to be priced at par. Another way to think of this is to imagine that the price of a bond today is made of a bundle of investments, each of which will grow at the prevailing interest rate to the value of the future coupons and the final principal. So, what would happen to the price of the bond if the prevailing interest rate was 12% i.e higher than the coupon rate of 10%? Well now, because each investment in the bundle grows at 12% instead of 10%, the value of the total bundle of investments or the bond price today should be less than £100. It will be around £96. The bond price is, therefore, inversely related to the bond’s –yield. Bond, notes, and bills are just different terminologies for US Treasury IOU’s that have different maturity dates. Bonds are long-dated notes of 10 years or more, bills are for up to a year and notes fit snugly in between.

Como o preço do título é efetuado pelos preços das ações? crise. Portanto, podemos dizer que os rendimentos geralmente seguem os desbotamentos de acionamentos de ações da empresa.

If there is a buoyant stock market, new bond issuers are forced to offer higher returns or yields to attract equity investors away from the stock market which would mean that existing bond prices would get cheaper and the converse is true in an economic downturn. So, we can say that yields usually follow the business’ stock cycles woes.

Como o déficit orçamentário afeta os preços dos títulos? Em tempos de déficit, o governo toma emprestado através de questões de títulos institucionais e os rendimentos devem ser maiores por causa da demanda e isso deve, por sua vez, tornar os títulos existentes mais baratos. O FMI publicou um documento de trabalho em agosto de 2010, examinando a relação entre os rendimentos da dívida de So Vereign e os déficits fiscais e os níveis de dívida do governo e o estudo revelou que níveis mais altos de dívida levaram a aumentos nas taxas de juros. No entanto, no caso dos EUA, descobrimos que isso não é verdade, mesmo que a dívida dos EUA tenha dobrado durante a última década para US $ 24TN, de 125% do PIB para 135%, os rendimentos dos tesouros de 10 anos caíram de 3% para 0,6%. Houve alguma correlação positiva entre os níveis de dívida e os rendimentos entre 2016 e 2018, mas depois de 2018, quando os níveis de dívida continuavam subindo, os rendimentos continuavam caindo. A direção e o nível dos rendimentos nos dizem que o mercado de títulos não está confiante sobre as perspectivas econômicas de longo prazo para os EUA e já esperava algum tipo de recessão antes da Covid 19.

The US has been experiencing deficits almost every year since the ’60s though, notably there were four consecutive years of surplus during Clinton’s tenure between 1998 and 2001 coinciding with peak employment levels. In times of deficit, the government borrows through institutional bond issues and the yields ought to be higher because of demand and this should, in turn, make existing bonds cheaper. The IMF published a working paper in August 2010 examining the relationship between so vereign debt yields and fiscal deficits and levels of government debt and the study revealed that higher levels of debt led to increases in interest rates. However, in the case of the USA, we find this is not true as even though US debt has doubled during the last decade to $24tn, from 125% of GDP to 135%, the yields on 10 year Treasuries fell from 3% to 0.6%. There was some positive correlation between debt levels and yields between 2016 and 2018 but after 2018, when debt levels kept climbing, yields kept falling. The direction and level of yields tell us that the bond market is not confident about the long term economic outlook for the US and was already expecting some sort of recession before COVID 19.

Monopólio e todos devem ser igualmente recompensados? Eu gosto de chamar isso de dinheiro de "monopólio" após o famoso jogo de tabuleiro. O jogo foi projetado por Elizabeth Magie, que nasceu em Illinois após o final da Guerra Civil dos EUA, em protesto contra os grandes monopolistas como Rockefeller e Carnegie de seu tempo. O que a maioria das pessoas não sabe foi que havia duas regras no jogo, as regras monopolistas e anti-monopolistas, mas hoje todo mundo se esqueceu do último. Ao contrário do primeiro, as regras anti-monopolistas garantiram que todos fossem igualmente recompensados quando a riqueza foi criada. Se um investidor comprasse tiras de 10% do tesouro com cupom zero de 10 anos, eles teriam alcançado um retorno, com pouco risco, próximo ao desempenho do S&P 500, que cresceu ininterrupto 8,5% ano após ano. O S&P continuou a subir, nivelando -se em 2000, quando o Tesouro ainda estava mostrando 8%. A comparação do desempenho entre títulos e estoques pode ser comparada a uma comparação entre um relé de cavalos (representando os títulos) e cães (representando as ações) correndo entre si contra o relógio através de matagais e florestas. O cão é ágil e mais rápido, mas sua vantagem natural também o torna mais propenso a cair e suscetível a obstáculos e ondulações do solo, mas os cavalos, embora mais lentos, são mais firmes, a menos que atinjam uma árvore! Sensibilidade do preço às mudanças nas taxas de juros. A Southwest Airlines, com sede em Dallas, é a maior companhia aérea orçamentária nos EUA por tamanho de passageiros e terceiro maior pela frota. Seu preço das ações caiu de US $ 50 para US $ 29 por causa da pandemia de Corona, que picou prematuramente a bolha de crédito agora familiar. Nos últimos trinta anos, a companhia aérea tem sido consistentemente rentável relatando US $ 400 milhões de receita líquida a cada trimestre, mas no primeiro trimestre de 2020, seu lucro líquido caiu imediatamente no vermelho. A empresa cortou seu estoque pela metade e tem uma perspectiva sombria. Mesmo assim, conseguiu arrecadar US $ 4 bilhões com a venda de ações e 1,25% 2025 notas de empréstimo conversível a um preço de conversão de US $ 38. As notas normais do empréstimo com a mesma maturidade têm um cupom de 5,25%. A Southwest tem a sorte de ter acumulado um baú de dinheiro em seu balanço, mas reconhece que isso será esgotado rapidamente, mesmo depois de recuar as despesas. Ele espera preencher apenas 9% de sua frota e não pode prever o ponto de lucratividade que essa companhia aérea de grande orçamento é um bom barômetro para a economia dos EUA, porque o transporte é o sistema nervoso da economia integrante ao trabalho e às empresas. mercado. A maior parte dos títulos dos EUA é absorvida quase igualmente pelos dívidas do Tesouro, Corporativo e Hipotecário, que juntas representam três quartos do total com dívida municipal (10%) e mercado monetário de curto prazo (3%) em frente. O economista Yardeni cunhou a frase "vigilantes de Bond" provocando uma imagem de cowboys sobrecarregados levando a lei em suas próprias mãos. Os Vigilantes de Bond conseguiram recuar contra a agenda de gastos fiscais de Clinton, vendendo suas participações que aumentam os rendimentos. O Dr. Alan Greenspan concordou que os Cowboys mantinham um domínio sobre o Tesouro, mas esse argumento agora está extinto, pois estamos testemunhando rendimentos baixos de todos os tempos em longos períodos de déficits fiscais. Alguns grandes jogadores. Os títulos do lado isento de impostos, ou títulos municipais ('títulos de Muni') são muito menores em tamanho e menos líquido e se movem no ritmo de um mercado exagerado. Os títulos podem pertencer diretamente ou mantidos por meio de fundos mútuos ou fundos negociados em bolsa (ETFs), que fornecem um preço único para um monte de fundos em que investem. Seja qual for o caso, cada um de segurança é identificado por um número especial chamado CESIP Code, um sistema de identificação de valores mobiliários na América do Norte. A propriedade de títulos individuais fornece mais flexibilidade, particularmente em momentos de volatilidade, quando os detentores correm para liquidar suas posições para obter dinheiro.

It is also interesting to note that 10-year yields fell sharply when the Fed decided to increase its balance sheet in 2008 in the hope of providing liquidity to the commercial banks and dealers in commercial paper. I like to call this ‘monopoly’ money after the famous board game. The game was designed by Elizabeth Magie, who was born in Illinois after the end of the US Civil War, in protest against the big monopolists like Rockefeller and Carnegie of her time. What most people don’t know was that there were two rules to the game, the monopolistic and the anti-monopolistic rules but today everyone has forgotten about the latter. Unlike the former, the anti-monopolistic rules made sure that everyone was equally rewarded when wealth was created.

Horses and Hounds

Ten-year Treasury yields have been gradually falling since their highs of 1980 when they stood at 14%. Had an investor purchased 10year 14% zero-coupon Treasury strips, they would have achieved a return, with little risk, close to the performance of the S&P 500 which grew uninterrupted 8.5% year on year. The S&P continued to soar, levelling out in 2000 by which time the Treasury was still showing a handsome 8%. The comparison of the performance between bonds and stocks can be likened to a comparison between a relay of horses (representing the bonds) and hounds (representing the equities) racing each other against the clock through thickets and forest. The hound is agile and faster but his natural advantage also makes him more prone to falling and susceptible to obstacles and undulations of the ground but the horses, though slower, are steadier, unless they hit a tree!

Airlines are a barometer of the US economy

Bond values are affected by several factors such as relative maturities, credit quality, and structure such as convertibility and call protection, and convexity which is the sensitivity of price to changes in interest rates. The Dallas based Southwest Airlines is the largest budget airline in the USA by passenger size and third-largest by fleet. Its stock price tanked from $50 to $29 because of the corona pandemic which prematurely pricked the now-familiar credit bubble. For the past thirty years, the airline has been consistently profitable reporting a whopping $400M of net income every quarter but in Q1 of 2020, its net income immediately fell into the red. The company cut its stock by half and has a grim outlook. Even still, it has managed to raise $4bn through the sale of shares and 1.25% 2025 convertible loan notes at a conversion price of $38. The normal loan notes with the same maturity have a coupon of 5.25%. Southwest is fortunate in that it had accumulated a war chest of cash on its balance sheet but acknowledges this will be depleted quickly even after stripping back expenditure. It is expecting to fill just 9% of its fleet and cannot predict the point of profitability This large budget airline is a good barometer to the US economy because transportation is the nervous system of the economy integral to work and businesses.

Vigilantes on horsebacks are a thing of the past?

The US bond market is worth around $40tn and is almost half the size of the global total and a third bigger than its sister US equities market. The major share of the US bonds is taken up almost equally by the treasury, corporate, and mortgage debt which together makes up three-quarters of the total with municipal debt (10%) and short-term money market (3%) trailing behind. The economist Yardeni coined the phrase ‘bond vigilantes’ eliciting an image of saddled cowboys taking the law into their own hands. The bond vigilantes managed to push back against Clinton’s fiscal spending agenda by selling off their holdings driving up yields. Dr. Alan Greenspan agreed that the cowboys had a hold over the Treasury but that argument is now defunct as we are witnessing all-time low yields in long periods of fiscal deficits.

Municipal and corporate bonds

A lot of portfolio management takes place at the level of corporate bonds also known as the ‘taxable sector’ where large volumes are traded electronically from screens by a few big players. Bonds on the tax-free side, or municipal bonds, (‘muni bonds’) are much smaller in size and less liquid and move at the pace of an over the counter market. Bonds can be owned directly or held through mutual funds or exchange-traded funds (ETF’s) which provide a single price for a bunch of funds they invest in. Whatever the case, each security each is identified by a special number called the CUSIP code, a North American securities identification system. Owning individual bonds provides more flexibility particularly at times of volatility when holders rush to liquidate their positions to get hold of cash.

Efeito do preço do petróleo em ações e títulos

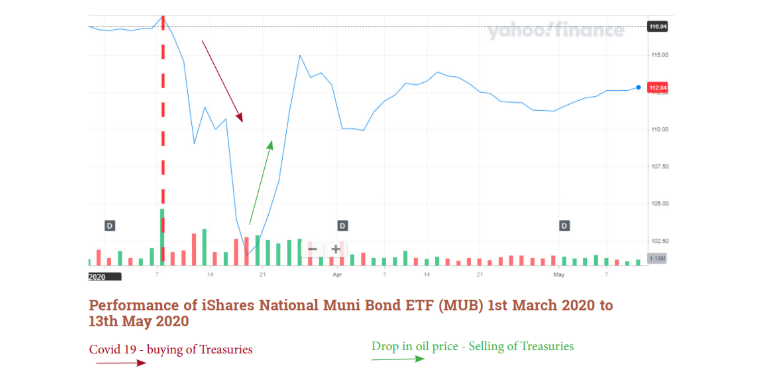

A queda acentuada dos preços do petróleo devido ao teto Saudi-Russiano para TAT começou no final de fevereiro de 2020, causou uma venda de ações e compra de fundos de títulos mútuos. Essa volatilidade repentina e grande impactou os hedgers no mercado de futuros de títulos que não conseguiram oferecer posições aos comerciantes devido à incerteza de preços. A ausência de visibilidade de preços impactou negativamente os valores de ativos líquidos dos fundos mútuos que, por sua vez, desencadearam uma venda e uma espiral descendente que durou duas semanas em meados de março de 2020 antes de uma revolta. Tesouro a favor dos investimentos do mercado monetário de curto prazo. A total return bond manager could have bought bonds in December 2019 and sold at the end of February 2020 and then bought again a few weeks after 9th March 2020.

The COVID 19 pandemic meant that equity investors were investing in the safety of bonds, backing the ‘horse’ instead of the ‘hound’ but then soon after when oil prices began to fall there was a sell-off of Treasuries in favor of the short-term money market investments. A total return bond manager could have bought bonds in December 2019 and sold at the end of February 2020 and then bought again a few weeks after 9th March 2020.

9th March 2020

9th March 2020 was the start of historic volatility in the US capital markets caused by the oil standoff between Saudia Arabia and Russia, both countries vying for a larger share of the oil market with the backdrop of COVID 19 e suprimiu a demanda mundial de petróleo e, no processo, criando um excelente excesso de petróleo que os navios -tanque estavam presos no mar, incapazes de descarregar sua carga de petróleo. Um movimento tão acentuado de preços não havia sido visto desde o acidente relacionado ao crédito do Lehman em setembro de 2008, que provocou uma venda de ações e a compra de pânico de tesouros deprimentes rendimentos até que eles se recuperassem no segundo trimestre de 2009. No entanto, o preço do petróleo em março de 2020 foi relacionado a liquidez e criou tanta volatilidade em que o Romes de Becada de Oil. Mercado?

What is the role of the Fed in supporting the money market?

Em 18/3/2020, o Fed estabeleceu uma instalação de liquidez para apoiar os fundos do mercado monetário (MMF) que investem em notas de curto prazo tipicamente receita e antecipação de títulos ou RAN e BAN. O Boston Fed fornecerá uma linha de crédito garantida aos bancos para comprar notas de grau de investimento dos MMFs para manter a liquidez no momento em que esses fundos estão passando por chamadas de resgate. Os EUA também estabeleceram, através do Fed, um termo de ativos de valores mobiliários (TALF). O Tesouro está indiretamente emprestando aos fabricantes de mercado para comprar e vender dívidas municipais de grau de investimento. Novamente, injetar liquidez em um mercado gelado e subscrever quaisquer perdas de estados inadimplentes. O programa TALF evita a questão espinhosa do tesouro se comportar como cobrador de dívidas. O dinheiro será usado para estabilizar os mercados de longo prazo em títulos de grau de investimento. O balanço do Fed estava em US $ 4,2TN no início de março de 2020 e agora custa US $ 6,7TN, a maior parte do aumento está relacionada à aquisição de títulos lastreados em hipotecas garantidas por Fannie Mae, Freddie Mac e Ginnie Mae. Isso soa familiar?

E os padrões de títulos? Isso significa que os títulos ficarão mais baratos e vimos isso, por exemplo, no preço do título chamável MTA 2034 da cidade de Nova York, onde as taxas de rendimento estão ligeiramente acima das taxas de cupom de 5%. Veremos muito interesse em tais tipos de títulos com taxas relativamente atraentes e superando o ETF MUB. Os títulos de alta qualidade estão fornecendo cerca de 3% de rendimentos que podem ser ajustados para cima, dependendo dos dados econômicos e possíveis rebaixamentos nas classificações e deterioração da cobertura do serviço da dívida, mas ainda parecem baratos quando comparados aos títulos longos que estão sendo negociados na metade desses rendimentos. MEER & CO

We should not expect any defaults on the investment-grade General Obligation bond (GOB) issuances from the larger states in the US such as New York or Washington however, there will be downgrading of credit ratings and thinner debt service coverages in the future. This means that bonds will get cheaper and we saw this, for example, in the price of New York City’s MTA 2034 callable bond where yield rates are slightly above the 5% coupon rates. We will see a lot of interest in such types of bonds with relatively attractive rates and outperforming the MUB ETF. The high-grade bonds are delivering around 3% yields which may be adjusted upwards depending on the economic data and possible downgrading in ratings and deteriorating debt service coverage but still seem cheap when compared to the long bonds which are trading at under half these yields.